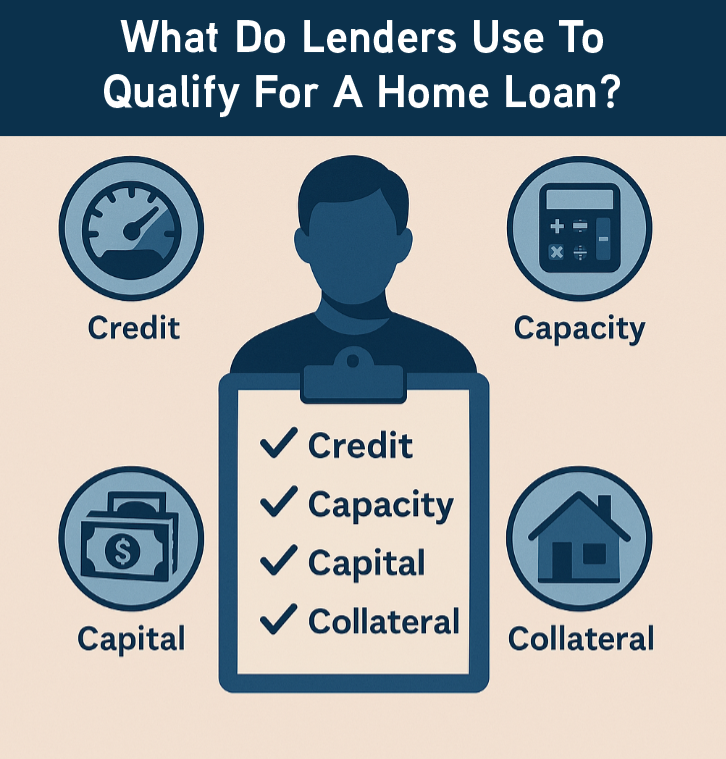

Question: What are the 4 C’s lenders use to qualify borrowers’ for a mortgage?

Answer: When applying for a mortgage, lenders evaluate your financial profile using the “4 Cs”: Credit, Capacity, Capital, and Collateral. Understanding these can boost your approval odds.

Credit: Your credit score and history reflect your debt management. A score above 670 (FICO) is ideal. Lenders check payment history, credit utilization, and inquiries. Improve your score by paying bills on time and reducing debt (Experian, 2025).

Capacity: This measures your ability to repay based on income and debt-to-income ratio (DTI), ideally below 43%. Stable employment (two years minimum) and consistent income are key. Pay down debts to strengthen capacity (CFPB, 2025).

Capital: Lenders assess your savings for the down payment and reserves. A 20% down payment avoids private mortgage insurance, and reserves ensure financial stability. Save early to show readiness (Fannie Mae, 2025).

Collateral: The property secures the loan. An appraisal confirms its value and condition, ensuring it covers the loan amount. Choose a well-maintained home in a stable market (HUD, 2025).

The 4 Cs gauge lending risk. Strengthen them by checking your credit, lowering DTI, saving more, and selecting a solid property. Consult a loan officer for guidance.

Sources: Experian, CFPB, Fannie Mae, HUD

We are ready to help you find the best possible mortgage solution for your situation. Contact Sheila Siegel at Synergy Financial Group today.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}